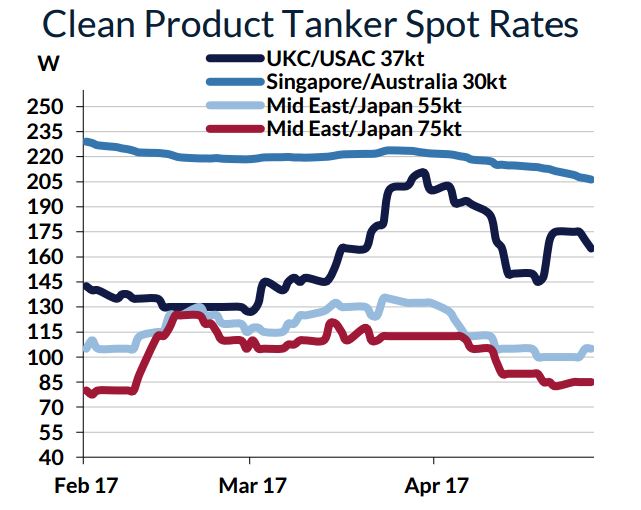

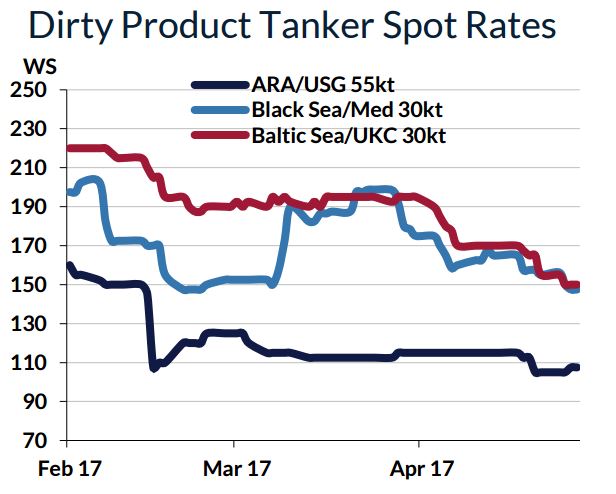

Product Tanker Demand Could Receive Boost from Turn of Shipping To Cleaner Fuels

TIN news: Shipping is bound for a “seismic” shift in terms of fuel supply for the global fleet, from 2020 onwards. While this is, on its own merit, a major event, it could also trigger a shift in demand patterns for the clean tanker fleet as well. In its latest weekly report, shipbroker Gibson said that “much research (including our own) has looked at the impact of the change in the global bunker specification from a compliance perspective. Whilst the debate as to what will emerge as the dominant option in the long term still rages, few doubt that middle distillates will (at least initially) emerge as the primary route to compliance. However, as significant as the impact will be from an operational perspective, attention should also be focused upon the trading opportunities that such a seismic shift creates”.

According to Gibson, “the IEA predict that middle distillates demand (excluding bunker demand) will grow by 1.9 million barrels by 2020, whilst refining throughput will grow by 3.9 million b/d. Whilst the IEA does not specifically state their assumptions for the increase in middle distillates demand directly linked to the specification change, a figure of 2 million b/d has emerged as a consensus among many analysts, indicating a very tight and perhaps even short gasoil market at the time. Such tightness is likely to generate interregional imbalances and pricing differentials, generating arbitrage opportunities for traders, and with that, freight volatility in the product tanker market”.

The shipbroker added that “in the run up to 2020, new refining capacity additions in the Middle and Far East start to emerge. 2019 is expected to see the start-up of Saudi Arabia’s 400,000 b/d Jizan refinery which will be well placed to ship middle distillates both East and West. However, other major Middle Eastern projects are likely to miss the start of the 2020 party, meaning the existing infrastructure, capacity upgrades, and capacity expansions in other regions (mainly Asia) will need to contribute to the global distillates pool. However, all regions will see a significant demand shift at the time, with only the Middle East, Russia and the US likely to have any surplus product for export”.

For clean tankers, these developments are clearly supportive from a demand perspective through the generation of new trade flows says Gibson. “However, the implications for dirty product tankers are harder to gauge and much will depend on where demand for what will be a surplus of fuel oil emerges. Much will depend on the eventual role scrubbers play, and how much of the excess fuel oil can be consumed for other purposes such as power generation, or as a low-cost feedstock to more complex refiners who have the facilities to handle it. Indeed, simple refineries with high fuel oil yields may be forced to rationalise capacity, and fuel oil production will be less attractive. This is likely to lead to less short haul trade within the developed OECD markets, with surplus volumes likely to be shipped into less developed nations. With increasing volumes likely to be shipped further afield, the decline volumes could be partially compensated for by longer voyages in terms of tonne mile demand. Equally, crude trading will be impacted, with sweeter crudes commanding a higher premium over the sour grades”, said Gibson.

It concluded its analysis by noting that “evidently from a clean tanker demand perspective, 2020 offers the potential for strong growth, whilst dirty product tankers face a more uncertain path. However, as we move into the next decade, the impact of new regulations is likely to push scrapping higher, particularly for older vessels which tend to trade more in the dirty products markets. Furthermore, just as we see a demand shift in the barrel, we could also witness a higher proportion of the younger dirty fleet migrating into the clean tanker market”.

Meanwhile, in the crude tanker market this week, in the Middle East, Gibson said that “VLCC market fizz faded as the week progressed and as Charterers moved onto better stocked forward positions. Rates have now fallen off an average 10 ws points to the East with ws 57.5 to the East and ws 34 to the West the current bottom markers. A long weekend for many now and that won’t aid any quick turnaround. Further erosion cannot be ruled out. Suezmaxes had a reasonably active week, but never reached a point of critical mass to leave rates in the mid/high ws 80’s to the East and low ws 40’s West. ‘Last done’ numbers seems to be the order of the day for the near term. Aframaxes broadly maintained their previous marks at around 80,000 by ws 115/117.5 to Singapore. but volumes were merely modest and the short-term outlook is flat”, the shipbroker concluded.

![AIRBUS A380 [MORE THAN 600 PASSENGER’S CAPACITY PLANE]](https://cdn.tinn.ir/thumbnail/4jCp4EQvCU0b/IjHVrSYQrIAqIzXuTzADR7qLYX4idQT4nfq__26E5SCUPLMqfhWkWajvuO9Wfq1ql1TjV4dhkrHliNQU82kMpo2NNftT_NGEwHc9KXtN_rk731bmifa2IQ,,/airbus-a380-structure1.jpg)

Send Comment